EMV Information

EMV Fifth Update - 03/09/2017

A new EMV update has been released from NCR that is positive and proactive. We just returned from NCR’s annual Focus convention where they addressed and communicated updates about new technology coming for both software and hardware.

The software information focused on EMV. They provided some insight regarding the next Aloha version which is scheduled to become a general release sometime this year. Lastly, there is a Kiosk station now available with both software and hardware offerings. There are prerequisites that are required to implement this solution.

Hardware: new tablets will be offered both wired and wireless with a release date in the near future. Aloha Kitchen Video is out and gaining momentum. There are new controllers and software that are now available.

Lastly, NCR provided an overview on security, stressing the importance of proper network environment configurations and maintenance. Given that there will be wireless tablets, iPads, and wireless credit card readers; security needs to be at the top of the list when reviewing the infrastructure of the POS network.

The main topic was Aloha EMV. Aloha currently has 96 sites live and working with EMV through Connected Payments. There are two different devices available today and a third wireless device in testing. There are 5 current credit card processors processing through EMV. Quick Service is the leader with 92 sites and 4 sites running the Table Service software of Aloha. The Quick Service configuration is a straight forward card present transaction.

In moving forward with EMV and the environment being very new there are many factors that require review before moving a site forward. The sites that are successful are the vanilla Aloha configuration sites not requiring advanced hardware and do not run additional modules attached to the system. Third Party software or products are not recommended to be integrated at this time.

The wireless credit card devices going to the table are still in testing. All working devices are tethered “cabled” to the terminal. Meaning, if the chip in the card, is required to be used to complete the transaction the patron will need to physically touch the device to complete the transaction. The patron will need to physically be in front of the device. Quick Service facilitates this as the patron is placing an order in front of the device. Think Home Depot or CVS style transaction. Currently, Digital Signature is still being developed which will in turn produce an emailed receipt. These solutions are on the roadmap. Given the current status, Quick Service is the target implementation environment as the software is rolled out into general release.

Factors to consider for Table Service at this time are the following. NCR is working on Offline/ Store & Forward, which is known to the Aloha world as “Spooling”. The configuration is in place but having issues preventing new site roll out. Tips or Adjustments in the processing world is also a challenge at this time. The topics are being worked on and NCR delivers weekly updates on the progress. There have also been settlement issues. This is the batching of the credit cards at the end of the night. This is also preventing new site roll out for table service at this time.

EMV software is making steps forward. The questions many ask is how is the USA so far behind. Well, we are not, we are the most complicated. The configuration of the transaction is more complex given the structure of the work force. The USA pays in tips while European countries offer a salary. Tips are not a consideration in the transaction in other parts of the world. Bar tabs are another consideration that is being requested that other parts of the world do not require, as such the software configuration has never been developed and only now are we exposing the security requirements. NCR has Connected Payments working in 1000’s of locations – retail transaction configuration. The software is valid and it now needs to fit into the Aloha Table Service configuration with the proper security configuration encompassing payment protection for the patron.

The key to success is options. Although the time frame has been long and tedious, the option to pick and choose credit card processors is the key. In keeping with the core benefits of Aloha, NCR is creating a software that allows the end user to choose from multiple credit card processors to shop cost savings, while processing credit cards.

So, What Works? Currently, the Quick Service software EMV solution offers 5 credit card processors with No Adjustments. These credit card processors are: First Data, Vantiv, Chase, Elavon, and World Pay. Only 3 credit card processors with adjustments (Tips): First Data, Vantiv, and World Pay. Please note there are specific hardware terminals that work with specific credit card processors. The devices and credit card processors are not interchangeable at this time. Table Service is currently offering 3 credit card processors, with and without Adjustments: First Data, Vantiv, and World Pay. Vanilla Aloha Software Configuration.

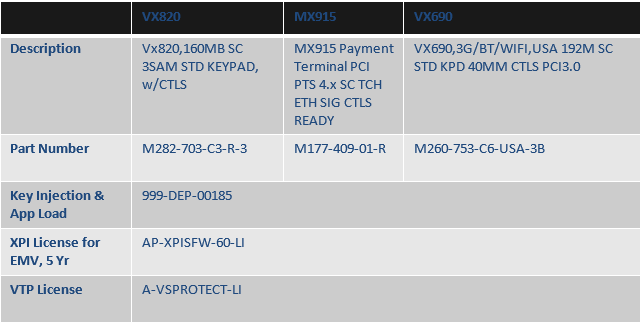

So what hardware works? Current devices are the MX915 and the VX820. Both of these devices “tether” to the terminal. The device needs to be powered either through a separate power supply or if the terminal has a powered USB, a power over USB cable. The wireless VX690 is still in testing. The MX915 device is geared toward the Quick Service market as it has a 5” video screen on it. Again, think CVS device. The VX820 looks like a silver bullet with a keypad

Points to keep in mind: These devices will need to be injected with an encryption key based on the credit card processor. Currently, these devices will be injected from the location of purchase – NCR. Programming them onsite or “reusing” a device is currently not available. Also, keep in mind once the wireless VX690 is available the site may want to have a VX820 on hand in case there is an issue with the wireless access point on property or as a back-up unit. Next step is site configuration with the EMV solution. There will be a “Global” change to the POS hardware. Meaning that the swipe on the terminal can be disabled. This segways the conversation to what other software will be affected by making a “global” change to EMV.

What software will be affected by going to EMV? This will be a case by case scenario to understand what software the site is running and advise to potential conflicts that will arise when making the advancement to EMV. Modules to be evaluated: All Third Party add on software involving payments or credit card interactions, Aloha To Go (ATO), Aloha Online Ordering, All Gift Card programs, All Loyalty programs, All Mobile Payment software, Aloha Mobile - iOS Devices and Orderman credit card swipes.

How all these software modules will be affected is still TBD for Table Service & Quick Service. As the EMV roll out occurs weekly updates from NCR are delivered to the dealer community.

So, what about pricing? Each site will evaluate the current challenges and find a launch point with EMV. NCR is offering Connected Payments as the software solution. EDC will not control credit card processing. Connected Payments will handle credit card processing and much more as time moves forward. The software will be offered as a Hosted Solution module with a setup fee and monthly cost. There will be a cost per device depending on what hardware the site chooses. Lastly, a service fee for programming, installation and training will be required. A quote is available through POSabilities today. A Site Survey is required to identify the current version of Aloha and hardware configurations. Once a quote is requested the site will be provided with the site survey results and recommendations for the system to accept EMV along with any challenges of any additional software modules identified.

Ok, So a quote has been received and still looking to move forward! Ordering timeframes. This will be a supply and demand driven process. I have been told orders can take up to 6-8 weeks to be delivered. This will take into effect the injection process and credit card processor configuration. The time frame is still an open scenario as it may be longer or shorter based on the market reaction to EMV. Keep in mind that the solution is still not in general release. Many want to be early adopters, many will want to play it safe and wait until the bugs are gone, and some will be completely off the band wagon. This will all affect the time frame for ordering gear. The next potential bottle neck will be the amount of orders into POSabilities. This will encompass the programming, installation, and training of the EMV software and devices. If the process is like adding a server into the system there is a 2 day per site scenario that occurs to work out the bugs. The market journals and the experienced professionals are advising that if a system has done nothing to prepare for the move to EMV it can take up to 6 months. From gathering info to processing options to pricing, system upgrades, training and EMV implementation a path well-worn will serve the end user well when accounting for the pennies, nickels, and dimes at the end of each day.

Recommendations! Start early. This is a phase one of options. As with all technology more options will arise. Learn as much as possible. Ask us questions. Acquire a site survey and a quote. This will help to evaluate the cost versus the price of EMV. What is the cost? chargebacks versus the price of moving the system into EMV status?

All of POSabilities sales reps are knowledgeable of the process and configuration requirements of EMV today. We are efforting to keep up with this ever-changing solution. We are here to move all sites to EMV at their pace as effectively and efficiently as possible.

EMV Fourth Update - 08/01/2016

Over the past few months, there has been a lot of development with EMV. Quick Service is ready to go and we are able to move forward with quoting and installing EMV ready Payment Terminals at these sites. The Table Service solution is still in the re-certification phase. This solution date is TBD, but close as the re-certification is underway. Since EMV for Table Service is not certified, we cannot provide this to you just yet.

EMV is a big shift in the way businesses will operate and by staying up to date with this topic you will be able to know whether this is the right solution for you. If you have not already done so, please read all of the information on our website and go through the Visa chip readiness guide.

"While the EMV testing and certification process is working its way across the U.S. payments landscape, Visa will also limit the number of transactions issuers can chargeback to merchants (and their acquirers) until April 2018. As of July 22, 2016, chargebacks under $25, due to U.S. counterfeit fraud, will no longer be charged back to merchants. Visa will block all U.S. counterfeit fraud chargebacks under $25. In addition to the dollars lost to fraud, the time and cost associated with managing those chargebacks is also onerous for merchants. As of Oct. 2016, Visa will also limit issuers to charging back 10 fraudulent counterfeit transactions per account. After that point, the issuer assumes liability." - (PYMTS.com 06/17/16)

The two articles below explain further how Visa and American Express take responsibility and make reprieves.

- Visa’s Merchant-Friendly EMV Moves

- American Express offers olive branch to merchants over EMV liability costs

We will continue to keep you updated on this topic as more updates become available.

EMV Third Update - 05/24/2016

This is our third EMV update for the Aloha community. It has been slow going but there is progress regardless of changes made by the card brands. The quality behind the Aloha solution is the open architecture and allowing for multiple credit card processor option. This offers the end user to approach the credit card processor from a strategic advantage in market selection.

When reviewing the current status of the industry one will find that still many retailers are not using EMV. Even Walmart is having difficulty moving forward and finding they too are in the mix of the charge back challenge. Now due to the challenges and delays congress is getting involved.

- Durbin Asks FTC to Explore EMV Certification Snags (external link)

There is also a growing movement toward legal action per the number of charge backs being allowed without any opportunity for rebuttal.

For some good news NCR is making forward movement with Aloha Connected Payments and the EMV solution. NCR has just gone live with a beta site on the Aloha Quick Service product. This solution is operational and being field tested. The solution is available starting at the end of June beginning of July. The solution has 5 processors to choose from: NCR -World Pay, First Data, Vantiv, Chase, & Elavon. The devices available are: VeriFone MX915 & MX925 for credit and debit.

As for Aloha Table Service – the solution has gone back into Re-certification. The card brands have made changes on their side that has required NCR to take the solution back through certification. This solution is slated to be available by end of July with limited functionality and limited devices. September is the target date for a wireless device to be available to bring to the table to complete the transaction. Please note this will all be a version 1 solution and many additional changes will be occurring moving forward.

For those who cannot wait any longer and want to be the first we do have pricing for software, hardware and services to configure a quote. Please note that when implementing new technology – the new technology will utilize the latest software platforms and require the latest hardware specifications. It is highly suggested that a site survey is requested to ensure the site is ready for a EMC Solution. Site surveys do take time so place your request today.

POSabilities is going through advanced training in the beginning of June and will have a fully configured test lab with firsthand knowledge of how the solution will operate by the middle of June. Our goal is to prepare the end user with as much knowledge possible as to what version 1 functionality will include and as important will not include. It is highly encouraged that all sites review EMV communications 1 & 2 as there is information and worksheets for the solution that are necessary to assist in making the right timed decision for a EMV implementation.

EMV Second Update - 10/21/2015

We are here at the second update for EMV and Aloha. If you have not watched the video or completed the liability worksheet included in the first update please keep those items top of mind. The decision to move to EMV is recommended to be based on the knowledge the change that EMV will have on the operations side of the business along with enhancing security and advancing today’s technology.

Up to this point many have seen that being ready to move forward is also a key component. Each site, per their request, has received a site survey of the business identifying each device, the specifications of those devices and the current Aloha software running at the site. In an effort to maximize the speed to EMV specific updates need to be confirmed before moving forward. The time is now to know where the system stands and make a plan for the next coming steps.

In this update we will discuss in more detail the software and hardware surrounding EMV within Aloha. This will also include the processors that Aloha has identified as the top five that will be incorporated into the solution. There will also be some critical thought given to the hardware that will be used, incorporating acquirement and replacement.

To begin it is essential to understand where the liability sits today given the changes that have taken place. Below is a graph that points out exactly where the merchant is liable.

This will help to ease the tension of the uncertainty and confusion that EMV inherently adds to the running of the business. Also note that EMV for the merchants offering payment option at the gas pumps or distribution of funds from bank ATM’s are not required to offer a chip solution till 2017. When reviewing all the timeframes it becomes apparent that the USA is still in a preliminary mode of informing and educating the general public on the expectations the chip card has on daily transactional payments. More importantly there is time to review and understand what is needed before a decision is made that may contradict the operation flow of the business.

NCR / Aloha is working to bring a robust EMV solution as quickly as possible. The goal is to offer a solution that keeps site of the importance of PCI Compliancy within a securely configured network while maintaining processor selection options within the credit card transactional landscape. To accomplish this NCR /Aloha is has created a software called Aloha Connect Payments. Aloha Connect Payments (ACP) – is a payment gateway that will be used to connect the credit card hardware to the POS terminal and create a software: Point 2 Point Encrypted tunnel for secure communication. The solution will also include the ability to use mobile wallets for payments as well. As this software becomes more developed for the hospitality industry the technology advancements and offering will become more robust. Items on the horizon will include digital signature, on-line ordering integration, along with loyalty and stored value. Aloha Connected payments is not new to NCR. This software has in place for many years servicing the retail sector. Currently there are over 17,000 users of this product today. The enhancement and changes are on the EMV incorporation of the software. The value within this software is the isolation from the POS, flexibility of processors and devices, tokenization security and easy adoption of new innovative payment methods as they arise.

Aloha Connect Payments is speculated as a hosted solution subscription service. The pricing is still being determined but is being described as a $150 set up fee and & $75 per month. The first release of the software is to provide Point to Point Encryption (P2Pe) and mobile wallet payment options with EMV integration with devices thereafter.

The flexibility of the solution NCR is working on will incorporate 5 processors. At this time the rollout is to be as follows:

- The first processor configured to run EMV will be RBS – World Pay. This is also NCR Merchant Services.

- The next 4 processor roll outs will be in the following order: First Data (BAMS) Rapid Connect, Vantiv-Fifth Third Bank, Chase Paymentech and Elavon.

- Additional processors will be added to the list per PCI & PADSS validation of the software and the hardware configurations.

The credit card hardware terminals will be available through the respective credit card processors. Due to the high level of demand and low levels of supply NCR is currently not a supplier of these devices. To obtain the device it will need to be purchased through the processor. The devices currently being used are:

- Verifone MX915 & MX925 – these devices are tethered to the terminal and ideal for quick service operations.

- Verifone VX820 – wireless device for table service operation looking for a “pay at the table” solution.

- Verifone VX690 - wireless device is still under development and will be the next device validated through the solution.

- Below are part numbers and additional software required for the device to work with ACP.

Keep in mind each EMV device requires an injected encryption (security codes/software) for the device to work with the specific processor to work. The injection may not come ready with the device when purchased and also may be additional to have completed. Purchasing these devices on the open market place may pose additional challenges to make them work once they enter into the business. Also keep in mind that if a device goes bad or is broken replacement may not be as simple as going to the store or calling the vendor to replace. The software injection may take multiple days before the device is ready for replacement.

For the next update we will discuss the differences between Chip and Signature and Chip and Pin. There will be a more in depth dive into the operational impacts that the EMV device will pose while running the business. There will also be the discussion of debit cards and taking advantage of the inherent value or cost savings accepting debit payment. Lastly, there will be the discussion about PCI security and what happens to these requirements once EMV is up and running.

Introduction - 09/22/2015

Here is the first of many updates regarding the EMV liability shift and more importantly Data Security that is recommended as the priority focus for the business. The information being presented comes from multiple sources within the hospitality and payment industries. The goal is to provide information on the EMV solution as it is still a work in process on all sides including – Consumers, Banks, Merchants and Processors. The key to moving forward is understanding everyone’s role.

Payment acceptance is changing rapidly and the security of the individual consumer, including their payment data, is taking a front row seat. To start: note that EMV is a transfer of liability - Not a deadline, nor a mandate. It is a relative point within payment data security. ATM machines and automated gas dispensers are not required to move to EMV till 2017. Note it is the Banks stating they are wanting to pass along the liability of a fraudulent charge by making all consumers use Chip credit cards and having the merchants use the EMV technology to process the payment. Keep in mind the consumers First have to have the cards. Here in the USA the number of issued chip cards are low but increasing. So the importance of EMV is high but the action ability of implementing EMV should be cautious.

The next area of notability is understanding chip & signature vs chip & pin. The USA is moving forward with chip & signature to start and then to chip & pin. But given the amount of credit cards issued from another countries, which have been configured as chip & pin, it is important that a solution selected has a chip & pin minded process. More details to be shared on this shortly. Due to the fact the EMV was coming to the USA many processors have created their process as chip & pin only and not chip & signature. So again before moving forward it is highly suggested you understand the rules of engagement, with the processor selected as the solution provider, on their details of EMV credit card processing.

Lastly, what is the effect EMV will have on the business’s operations? We highly suggest in personally engaging in a chip credit card transaction as quickly as possible to “feel” the new way a payment transaction occurs. First and foremost there will be a time delay in processing a credit card payment. The other areas being effected is the way the tip will be configured on the guests check. Remember EMV is a card present transaction. The total of the check must be completed in totality. Meaning the tip is processed with the payment before the card leaves the building. This is very different from today as a tip in many instances is not added for up to hours later. Also, if your business allowed for customers to run an open credit card tab – this functionality has changed for chip & signature and changed drastically for chip & pin.

Given that this is a lot of information on multiple topics we have included a video from NCR and RBS World Pay that will review the above points and others that are critical to the success of your business’s EMV and data security implementation.

EMV Introduction Video (external link)Please note that this video was optimized for use on mobile device and that the initial load is very slow at times. It also requires registration prior to watching the video.

After watching the video keep in mind that data security is the most important point and that EMV is only a portion of the solution. Below you will find information on the network environment PCI compliant solution and how to maintain PCI compliancy.

- PCI Security Plan (external link)

- PCI Security - Staying Compliant (external link)

If all this information is overwhelming you are not alone. With all kinds of questions about where and when to start it is important to ensure you are in control from the beginning. Below is a link to a self-evaluation worksheet that will help to identify what the business’s liability exposure during the time of review as to what approach to EMV is best for the business.

Lastly, we have included additional website links to payment news articles and information commenting and educating on data security and EMV.

Additional external links

The next communication will touch on when is the right time to go to EMV? After learning the vocabulary and understand the current landscape of the technology the next step is when to undertake the EMV initiative. EMV will bring about many new options to the hospitality payment world that has never been there before. For example – Digital signature, emailing of receipts, extended payment options and mobile phone payment options. When will all these options be available and which devices today will be obsolete next 6 -9 months? Stay tuned as this topic is only getting hotter!